Last month, we broke down the typical journey of an electricity buyer assessing a PPA strategy, from the initial reflection phase to contract management after signature. Beyond price: how to properly evaluate a PPA?

Today, we continue with the topic of PPAs but we focus on a very different aspect: the aggregator. What is its role? What services does it provide? And why can its intervention make it easier to integrate a PPA into a consumer’s electricity supply?

Before intervening in long-term renewable contracts, aggregators already have a clear role in an electricity system where the balance between generation and consumption must be maintained at all times. In the context of PPAs, their role is to create the link between intermittent renewable generation on the producer side and a consumer that wants to integrate this energy into its procurement strategy, with as much visibility as possible on volumes, prices and associated risks.

The aggregator: market access, but not only

The initial role of the aggregator is market access. The aggregator acts as an intermediary that facilitates transactions on the energy market while absorbing certain risks.

A renewable producer, especially one operating a small or medium-sized asset, does not always have the resources required to sell its electricity directly on wholesale markets. This is where the aggregator steps in as a specialised intermediary. It brings together several generation assets, flexible consumption assets or storage assets and integrates them into its portfolio in order to operate them. This mutualisation makes it possible to sell the electricity generated, optimise its market value and, in some cases, provide flexibility services to the electricity system.

We are seeing an increasingly favourable regulatory framework for the role of aggregators. For example, in Spain, last February, the government recognised the figure of the independent aggregator to integrate more flexibility and facilitate the active participation of consumers and small producers in the energy market under Real Decreto 88/2026. (More information here).

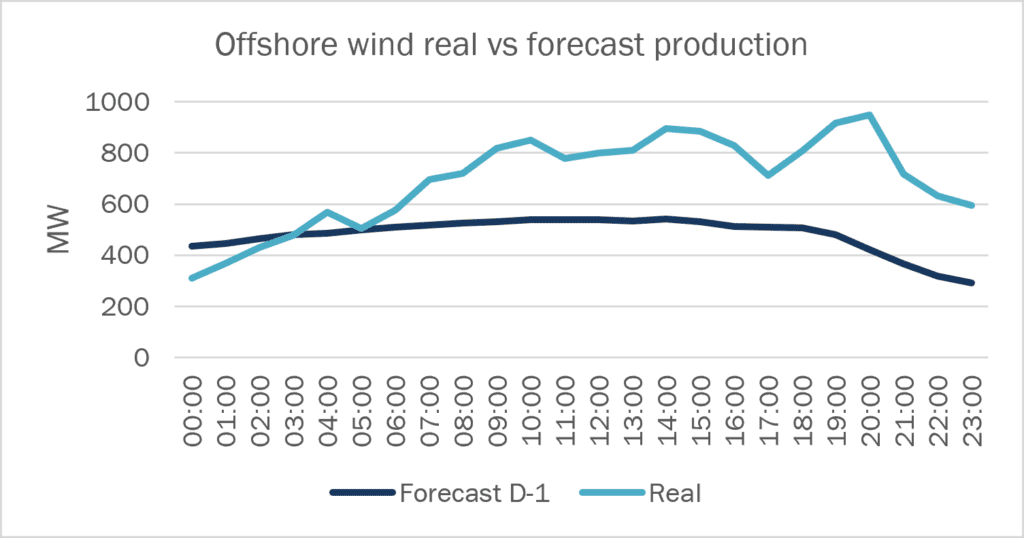

This role is becoming increasingly important with the growth of renewable energy. Deviations between forecast and actual generation can weigh on market balances. The aggregator is therefore not only an administrative intermediary: it is becoming an actor in the operational and economic management of variability.

Within a PPA, an integration role between producer, consumer and supplier

Several actors are involved in a PPA. The customer wants to decarbonise part of its consumption and secure a long-term price. The producer seeks to guarantee revenues in order to finance or make its renewable assets profitable. The supplier must continue to ensure the overall delivery of electricity to the consumer, including when that consumer has signed a PPA with a third-party producer. It is at this intersection that the aggregator can bring value.

It enables the volume generated under the PPA to be integrated into the customer’s overall supply architecture, taking into account market constraints, balancing rules and the variability of generation. This intervention can be more or less extensive. In some cases, the aggregator simply organises market access for the producer. In others, it takes responsibility for forecasting, imbalances, or even the transformation of the generation profile into a volume that is better adapted to the customer’s consumption profile, known as “shaping”. Each level of service corresponds to a different level of risk transferred to, and assumed by, the aggregator.

The risks an aggregator can manage – different levels of intervention

The first risk is imbalance risk. In the electricity system, injections and withdrawals must remain balanced. However, because renewable generation is intermittent by nature, there are variations between estimated and actual production. When an imbalance occurs, it generates a cost. The aggregator reduces these deviations between forecast and reality thanks to its forecasting models, its market experience and the size of its portfolio. For an isolated producer, a forecasting error has a direct impact and a financial cost. For an aggregator, that error is integrated into a broader set of assets, making it easier to anticipate, correct or offset. In this configuration, the aggregator no longer simply sells electricity; it seeks to anticipate actual generation as accurately as possible and takes responsibility for the costs linked to imbalances.

Figure 1 French offshore wind assets (MW) – RTE

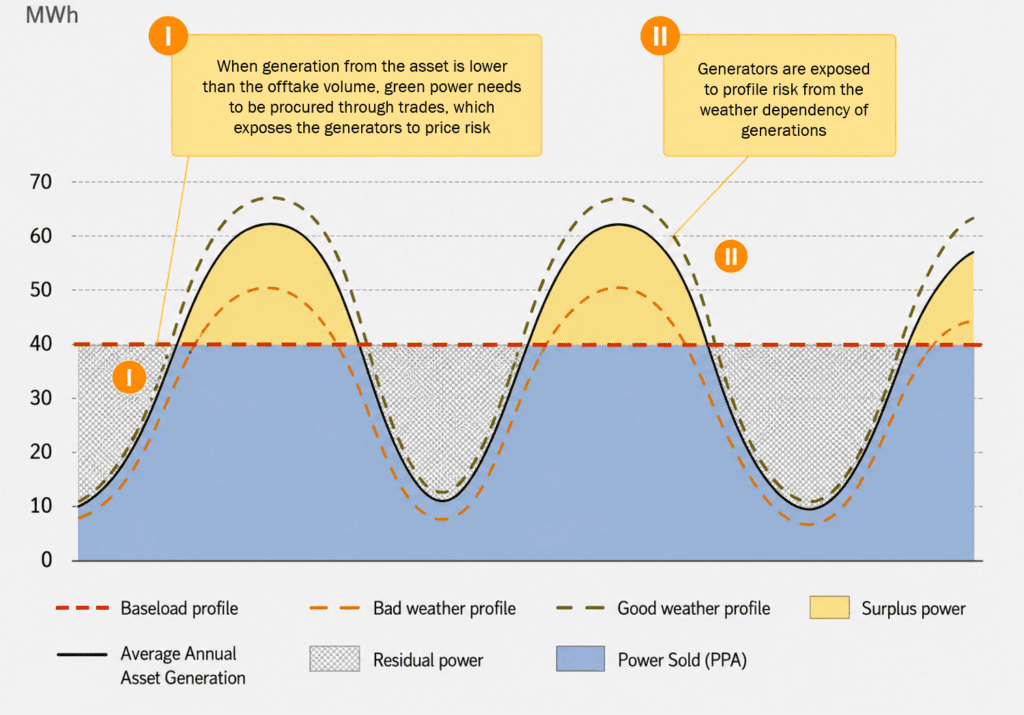

The second risk is volume risk. Even if P50 or P90 scenarios provide a statistical indication, actual generation will depend on real conditions. In an as-produced PPA, the consumer receives energy as it is generated. But in a baseload or as-consumed PPA with a fixed volume or predefined profile, deviations between injected generation and the committed consumption volume must be managed. This is where the aggregator intervenes by purchasing missing energy or reselling surplus volumes in order to deliver the defined product to the consumer. This service is particularly useful for producers that do not have sufficient tools to complete the volume when actual generation falls short.

Figure 2 : Illustrative supplier generation and offtaker demand under a baseload PPA (MWh) – Centrica Energy

The third level is more advanced: the aggregator transforms renewable generation into a structured product. This is profile risk, often referred to as shaping risk. A solar plant mainly produces during the day, following a “solar bell” shape. A wind farm may produce more irregularly, sometimes at night and sometimes during periods of low consumption. However, the consumer generally does not have the same consumption profile as the renewable asset. The role of shaping, managed by the aggregator, is therefore to transform as-produced generation, meaning electricity delivered as it is generated, into a more readable product: a baseload block or another profile adapted to the customer’s needs. This is a qualitative shift: the aggregator is no longer only providing an operational service; it is also taking an economic position on volumes, prices and the delivery profile. The more the final volume is reformatted or “shaped” by the aggregator, the greater the premium transferred.

Portfolio diversification: the aggregator’s foundation

One of the aggregator’s main levers is the diversification effect, often referred to in French as “foisonnement”. The idea is simple: when a single producer makes a forecasting error, that error is fully visible. But when several assets are grouped within the same portfolio, errors do not always move in the same direction. One asset may produce slightly less than expected, while another produces slightly more. For example, a solar plant in one region may be affected by cloud cover, while another plant located elsewhere is not.

Portfolio diversification does not eliminate all risks. In the event of a widespread weather event or a systemic price movement, the entire portfolio may be affected. But it does help reduce some individual forecasting errors and smooth variability. This is an essential difference between an isolated producer and an aggregator: the aggregator’s value does not rely solely on market access, but also on portfolio management and risk mutualisation.

What is the value for a consumer?

For a corporate buyer, the value of an aggregator depends on the structure of the PPA and how the contract is integrated into the broader electricity supply arrangement. Without an aggregator, several questions must be addressed directly between the producer, the consumer and the supplier. The supplier may also integrate the PPA into its own balancing perimeter, but this requires stronger contractual coordination with the producer and may limit the consumer’s flexibility in choosing its counterparties. The supplier may also favour producers already present in its own portfolio or propose pricing structures that reflect the costs and risks it is willing to carry.

With an aggregator, part of this complexity is delegated. The aggregator organises block exchanges, manages imbalances, structures renewable generation and facilitates its integration into the customer’s supply contract. For the buyer, this can offer greater freedom in choosing the producer, as the aggregator creates the link between the renewable asset and the existing supply arrangement.

How is the aggregator remunerated?

The aggregator’s remuneration depends on the role it plays in the contract. When it provides forecasting and imbalance management, the service price also reflects the cost of tools, teams, trading capabilities and the imbalance risk it agrees to carry. When it structures a more complex product, its remuneration is generally embedded in the price offered. It then reflects not only the service provided, but also the premium transferred: volume risk, price risk and profile risk. In practice, there is no single aggregation tariff. The economic value depends on the level of service, the technology concerned, the balancing perimeter, the quality of forecasts and market liquidity. This is why contractual transparency is important. To compare several offers, it is not enough to look at the final price; it is also necessary to understand what is included.

Conclusions

The development of PPAs and the growth of renewable energy make the role of aggregators increasingly strategic. They facilitate market access, improve imbalance management, mutualise risks within a portfolio and can transform variable generation into a product that is more compatible with a consumer’s needs.

But their role must be understood precisely. The aggregator does not make risk disappear; it assumes part of it. This risk-taking has a value, which is reflected in the price of the service.

For a consumer, the key challenge is therefore to choose the right level of intervention. An aggregator can make a PPA simpler to operate, easier to integrate into a supply contract and better adapted to the customer’s consumption profile. But the right structure will always depend on the objective pursued: securing a price, reducing market exposure, simplifying operational execution or obtaining a product that is closer to actual consumption.

Céline Haya Sauvage