Spanish Market Analysis

Analysis of the Spanish energy market is key to understanding the dynamics and trends affecting the sector both locally and internationally. In this detailed analysis, we address the important factors influencing energy prices, supply and demand, and the latest regulatory policies. This comprehensive overview will allow you to keep up to date with weekly changes and anticipate possible market variations, both in Spain and in other relevant markets such as France.

June 2026

Table of Contents

Key figures of the month

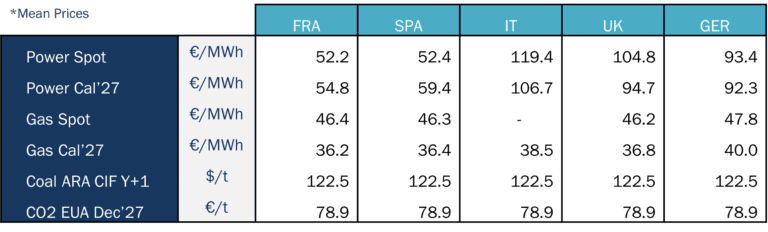

Source: Haya Energy Solutions

In May 2026, electricity spot prices across the main European markets increased compared with the previous month, with average monthly prices rising by more than 10 €/MWh in most countries. Italy was the main exception, remaining the highest-priced market in the region at broadly the same level as in April. In the forward market, however, Power Cal’27 remained relatively stable across all countries, although price levels moved within a slightly higher range than those observed in the previous month.

France and Spain were once again the lowest-priced power markets in the region, both averaging around 52 €/MWh, despite the increase recorded in their monthly average prices compared with April. By contrast, the rest of the main European markets remained at significantly higher levels, with Germany averaging close to 93 €/MWh, the UK reaching around 105 €/MWh, and Italy remaining near 120 €/MWh. Overall, May once again highlighted the wide divergence in spot prices across Europe, largely reflecting each market’s renewable generation profile and, in particular, its degree of exposure to gas-fired technologies as the marginal price-setting source.

From a pricing perspective, one of the most notable developments of the month was the record low daily average price registered in the French market on 1 May, which fell to -41.39 €/MWh. This was mainly driven by lower electricity demand associated with the public holiday, combined with favourable conditions for solar PV generation.

More broadly, May was also a record month for solar PV output across several major European markets. New all-time daily highs for the month of May were reached in Germany (503 GWh), Spain (265 GWh), France (179 GWh) and Italy (161 GWh). This strong solar performance reinforced downward pressure on prices during central daylight hours, particularly on days when high renewable generation coincided with softer demand.

On the gas side, average spot prices remained broadly stable around the 46 €/MWh mark across most markets, with Germany standing slightly higher at around 48 €/MWh on average. Compared with April, gas prices posted a modest increase across all countries, rising by around 2 €/MWh in most markets. Gas Cal’27 also showed a slight month-on-month increase across all countries.

As has been the case since the outbreak of the conflict, gas price formation remained largely driven by developments involving Iran, Israel and the United States, and, in particular, by events affecting the transit of gas and oil through the Strait of Hormuz. At present, the conflict appears to be in an open phase of negotiations aimed at de-escalation, while the ceasefire remains in place but highly fragile, with sporadic attacks still being reported. In this context, any signal ranging from progress in the talks to renewed disruption risk continued to feed directly into gas prices.

As for CO₂, prices increased from around 77 €/t in April to 79 €/t in May, extending the upward trend that had started in the previous month. The move appears to reflect sentiment and geopolitical risk more than a significant change in near-term fundamentals.

Overall, higher gas and CO₂ prices contributed to renewed upward pressure on electricity markets in May, partly offsetting the downward effect of strong solar generation across Europe.

Energy demand and generation mix

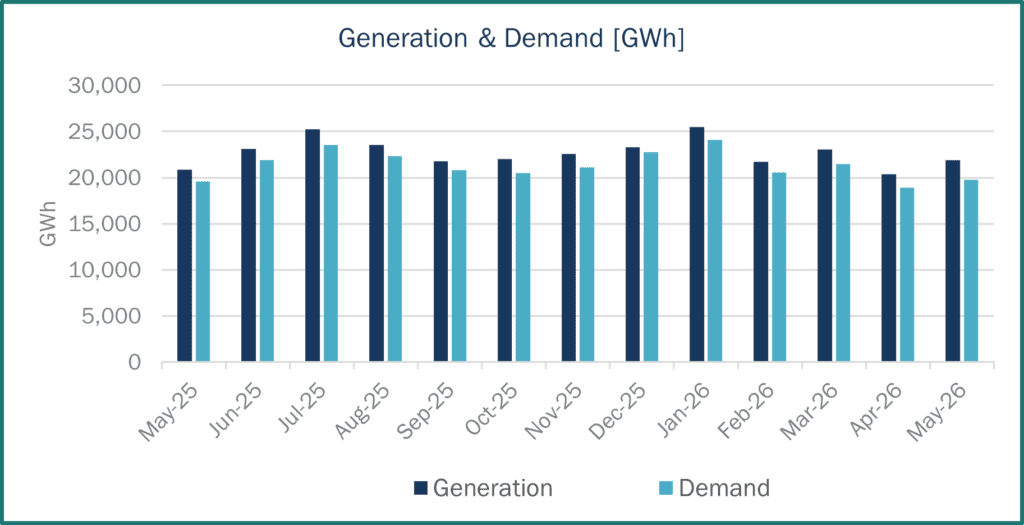

Source: Haya Energy Solutions

Spanish electricity demand reached 19,783 GWh in May 2026, while total generation stood at 21,907 GWh. Of this volume, around 2,124 GWh was scheduled for export.

Compared with April 2026, both electricity demand and generation increased. On a year-on-year basis, demand and generation were also higher than the levels recorded in May 2025.

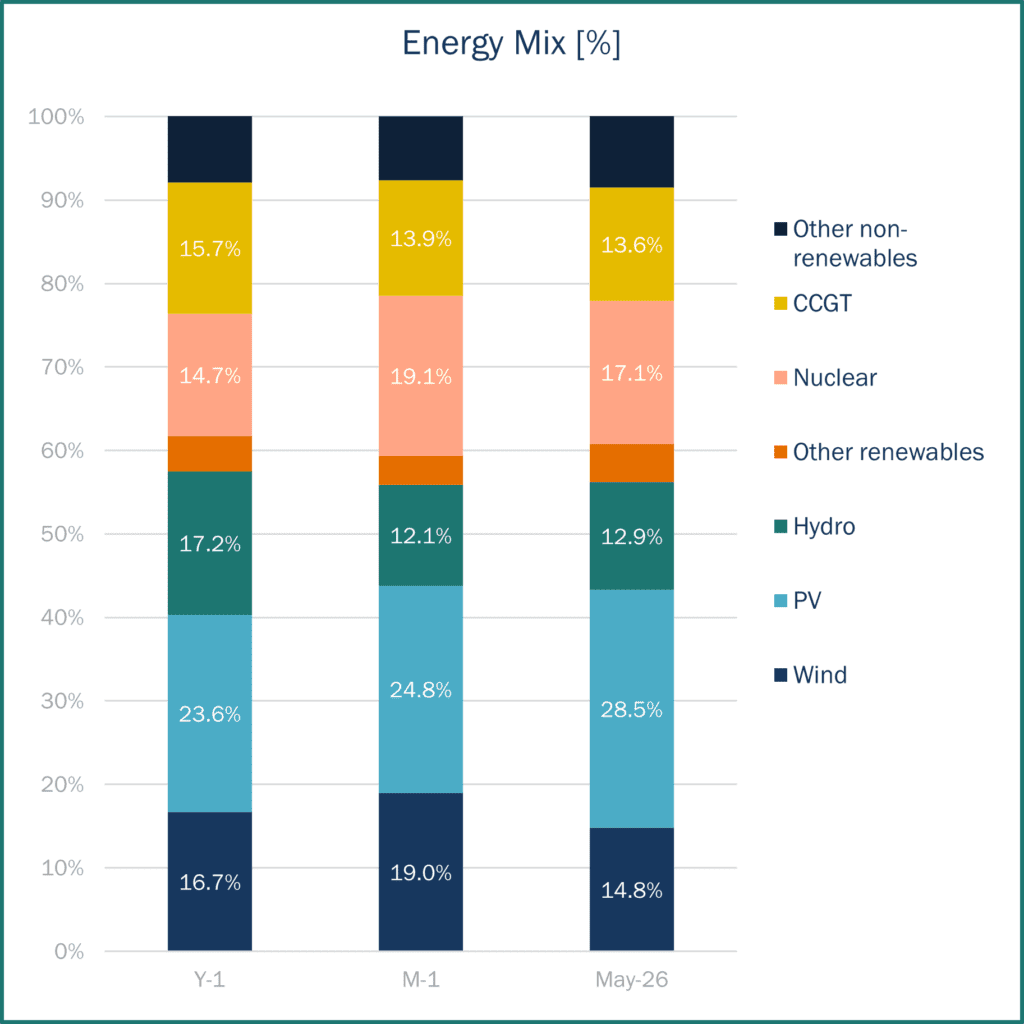

Renewables represented 60.5% of Spain’s generation mix in May 2026, up from 59.3% in April 2026, but still below the 61.6% recorded in May 2025. Solar PV remained the leading generation source, accounting for 28.5% of total output. This was above both April 2026 (24.8%) and May 2025 (23.6%).

Nuclear retained its position as the second-largest generation source, reaching 17.1% of total output, slightly below the 19.1% recorded in the previous month. The main developments for this technology during May were the completion of the 31st refuelling outage at Almaraz Unit 1 on 14 May, marking the start of what could be its final operating cycle under the current nuclear phase-out calendar, and the disconnection of Ascó I from the grid on 8 May to begin its own 31st refuelling outage.

Wind ranked third, contributing 14.8% of total generation, below both April 2026 (19.0%) and May 2025 (16.7%).

Overall, one of the most notable features of the month was the clear dominance of solar PV in Spain’s generation mix. With a 28.5% share, it remained well ahead of nuclear (17.1%) and almost doubled the contribution of wind (14.8%). In addition, wind moved at levels closer to those of hydropower (12.9%) and CCGTs (13.6%), further underlining the particularly strong role played by solar generation during the month.

Source: Haya Energy Solutions

Energy prices & market panorama

Source: Haya Energy Solutions

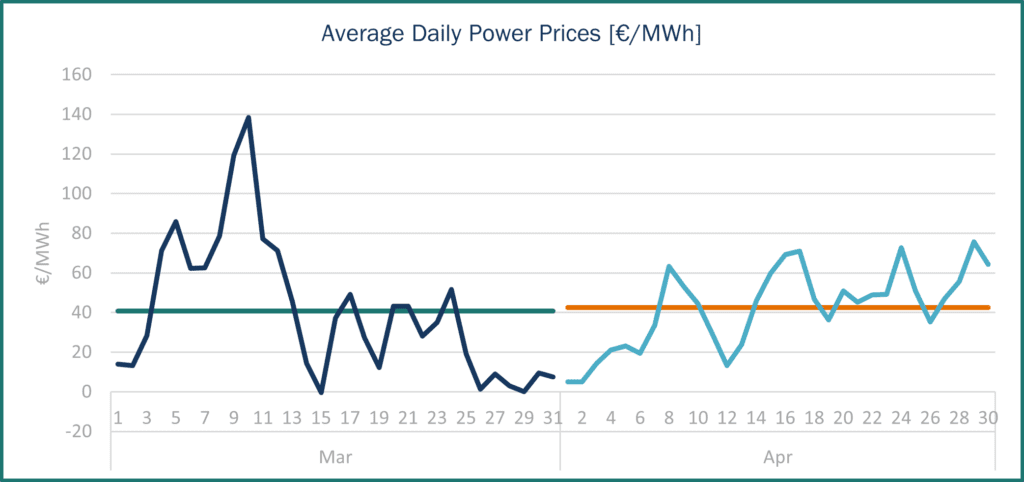

Spain’s average wholesale electricity price stood at 54.23 €/MWh in May 2026, above the 42.44 €/MWh recorded in April. As in the previous month, the most notable feature from a pricing perspective was the persistence of a clear intraday pattern: electricity prices fell to near-zero, or even negative levels, during hours of strong solar generation, before rising sharply once solar output faded.

Looking at the daily average price profile, significant swings were observed within just a few days. For example, the daily average price came close to 87 €/MWh on 7 May, while only three days later, on 10 May, it stood at just above 20 €/MWh. More broadly, the distribution of daily prices shows two clear peaks, one at the beginning of the month and another towards the end, while prices remained more clustered around the monthly average during the central part of May.

This pattern reflects the high level of renewable penetration in Spain, particularly solar PV, which continued to exert strong downward pressure on prices during the central hours of the day. However, as solar generation declined towards the evening, the system increasingly relied on other technologies to meet demand, including gas-fired plants such as CCGTs, which could trigger sharp price increases within a short period of time.

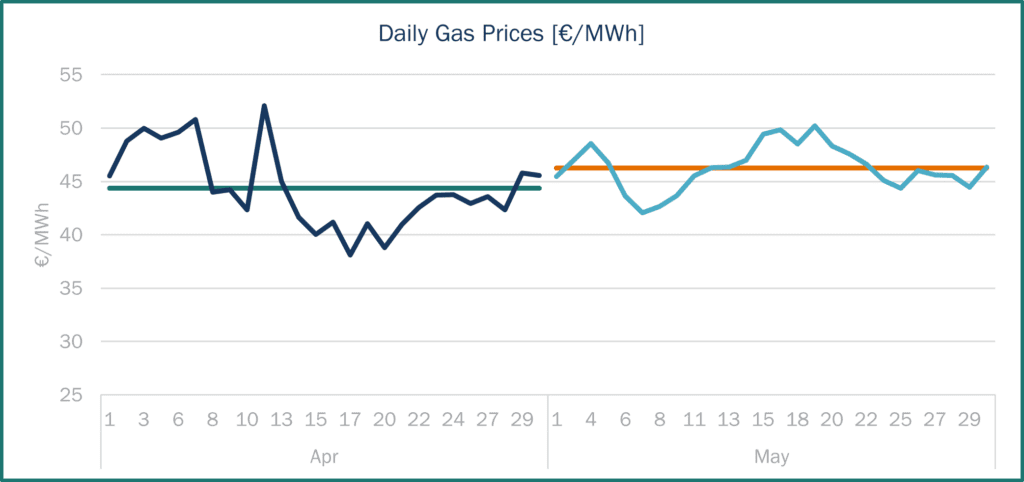

The average natural gas price in the Spanish market stood at 46.25 €/MWh in May 2026, up from 44.36 €/MWh in April, although still broadly stable on a monthly average basis.

As has been highlighted in previous months, gas prices remained closely linked to developments in the Middle East conflict. However, compared with earlier periods, price movements during May were less pronounced.

Source: Haya Energy Solutions

During the first days of the month, gas prices followed a downward trend, reaching the monthly low of 42.05 €/MWh on 7 May. This pattern shifted after a renewed escalation in tensions, following reports that the United States had destroyed six small Iranian vessels after attacks on commercial ships, while the United Arab Emirates reported Iranian missile and drone attacks.

These developments triggered a renewed upward trend in gas prices, which peaked at 50.22 €/MWh on 19 May, the highest level of the month. From that point onwards, prices gradually eased again towards month-end, supported by renewed hopes of a US-Iran agreement that could lead to the reopening of the Strait of Hormuz.

Overall, gas price formation remained highly sensitive to geopolitical headlines, although volatility was lower than in previous months.

Market trends and futures

Source: Haya Energy Solutions

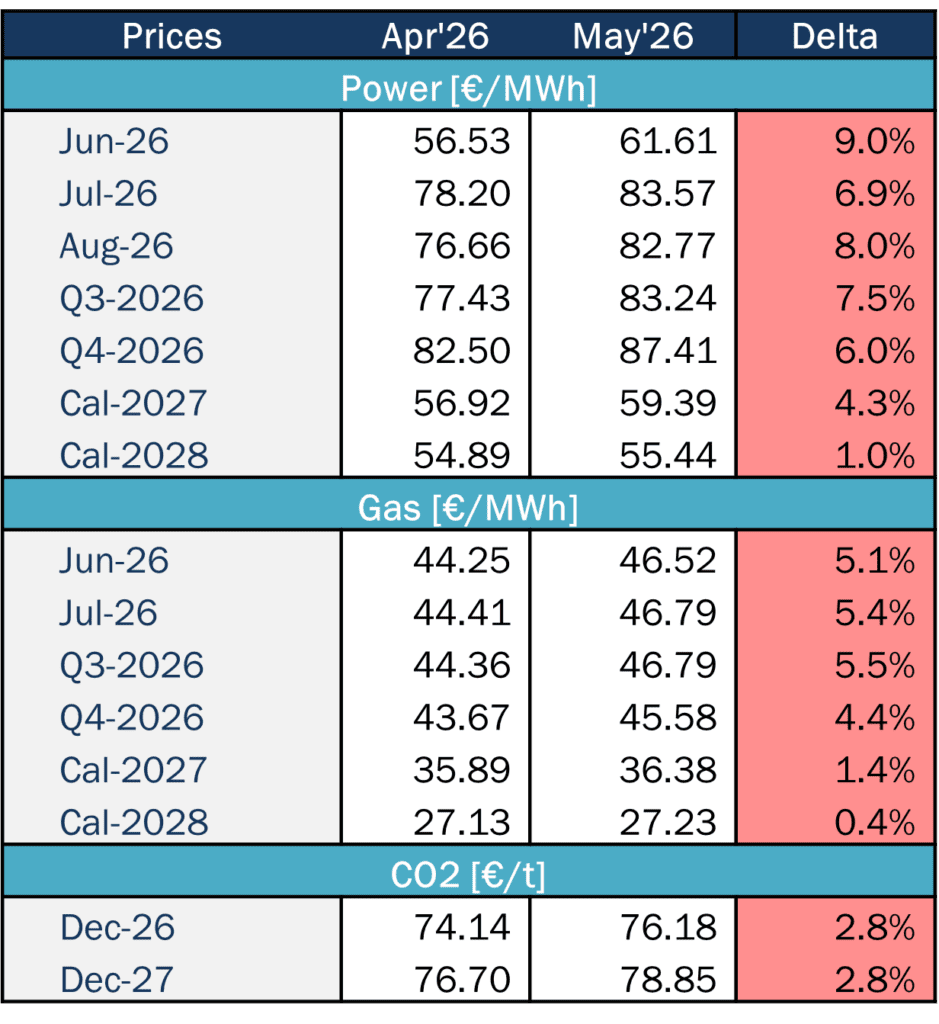

Spanish electricity forward prices moved higher across all products in May 2026 compared with the previous month. The increase was more pronounced in the shorter-term contracts, with the most notable moves being the 9.0% rise in the June 2026 product and the 8.0% increase in August 2026. More broadly, the upward repricing was visible across all power forward products, confirming a generalised increase in wholesale electricity price expectations.

In the gas market, month-on-month increases were also observed across all the products under review. Forward gas prices for June 2026, July 2026 and Q3 2026 rose by more than 5% compared with the previous month. A similar upward movement was also seen in Q4 2026, although the increase became much more limited in the longer-term products, with Y+1 rising by around 1.4% and Y+2 by just 0.4%. This suggests that, while short-term gas prices remained sensitive to geopolitical developments, the market continued to price in some degree of easing in the conflict over the medium to longer term.

Regarding storage levels, natural gas reserves in the European Union currently stand at 40.09% of capacity, an increase of around 7 percentage points compared with the previous month. In cumulative terms, European gas storage levels have risen by more than 13 percentage points over the last two months. Although inventories remain relatively low for this stage of the year, the recent trend is clearly positive. The European Union therefore continues to rebuild gas stocks in order to reduce its exposure to potential price tensions ahead of next winter. In Spain, gas reserves currently stand at 70.35%, around 6% above the previous month and still well above the EU average.

CO₂ also moved higher during the month, marking its second consecutive monthly increase. Fundamentally, however, the EUA market remained relatively stable. The European Commission’s benchmark revisions appear to have had only a limited impact on the medium-term ETS balance, while relatively high temperatures and strong renewable output continued to constrain thermal generation and power-sector emissions. In this context, the rise in EUA prices seems to reflect sentiment, policy uncertainty and geopolitical risk more than any meaningful tightening in short-term market fundamentals.