A practical guide to understanding how to assess a PPA from a market, risk, and energy strategy perspective.

In a context of volatile energy prices, growing sustainability pressure, and the need to secure competitive energy costs, Power Purchase Agreements (PPAs) have become an increasingly important instrument for industrial and commercial consumers.

But how does a buyer actually approach the decision to sign a PPA?

What questions should be asked before committing to a long-term agreement?

Which risks should be assessed from the outset?

In this newsletter, we follow the typical journey of an electricity buyer evaluating a PPA strategy — from the initial reflection phase to contract management after signature.

Far from being simply “renewable energy at a fixed price,” a PPA is a strategic decision that directly impacts how a company manages energy risk, procurement costs, and long-term market exposure.

Understanding the real value of a PPA requires going beyond headline pricing. Buyers must assess contract structure, consumption profile matching, market scenarios, balancing costs, and risk allocation to determine whether the agreement truly supports their energy and business strategy.

(If the reader would like a preliminary introduction to PPAs, they can visit our webpage Key information on PPAs.)

Why Consider a PPA?

The answer is not immediate. A PPA is not simply “renewable energy at a fixed price.” It is a strategic decision that directly impacts how a company manages energy risk, procurement costs, and long-term exposure to electricity markets.

Today, most consumers purchase electricity through suppliers, combining spot-indexed procurement with short-term hedging products. While this model provides flexibility, it also creates uncertainty: energy costs may vary significantly from one year to another depending on the evolution of electricity, gas, and CO₂ markets.

In this context, PPAs emerge as an alternative capable of providing greater stability and visibility.

The main value proposition of a PPA is clear: securing a long-term price reference while reducing exposure to electricity market volatility. For many industrial consumers, this improves budget predictability and reduces sensitivity to market shocks.

In addition, buyers can access this stability without directly investing in generation assets, while simultaneously contributing to electricity decarbonization and supporting ESG objectives.

However, a PPA does not eliminate risk it transforms it. A PPA involves a long-term contractual commitment and potentially exposes the buyer to new risks, including market price declines that make the agreed price less competitive, operational risks related to the producer, or counterparty risk in long-duration contracts.

What Type of PPA Should Be Chosen?

Once the decision to explore a PPA has been made, the next key question is: what contractual structure best fits the consumer’s profile and objectives?

There is no single model. The optimal structure depends on the desired level of coverage, risk tolerance, and the company’s overall energy strategy.

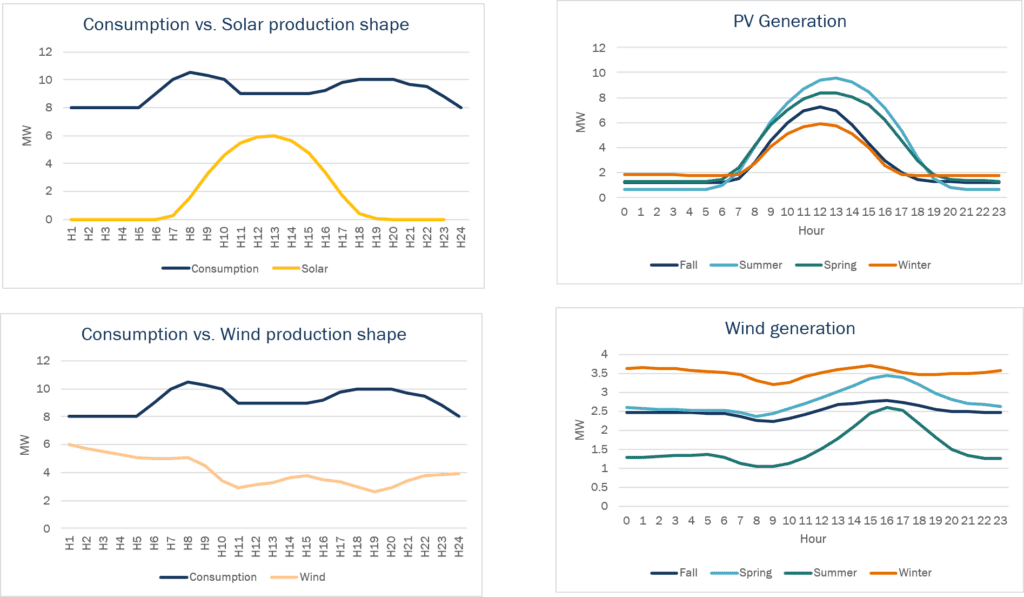

One of the first aspects to assess is the degree of alignment between the renewable generation profile associated with the PPA and the buyer’s actual consumption profile. The stronger this alignment, the greater the economic value of the contract and the lower the exposure to surplus energy sales under unfavorable market conditions.

For example, predominantly daytime consumption typically aligns better with solar PPAs, while more stable consumption profiles may require wind generation or a combination of technologies to achieve more efficient coverage.

Another key factor is the contract’s time horizon. PPA duration generally depends on several elements, including the need for budget visibility, industrial strategy, and expectations regarding future electricity market evolution. In general terms, contracts may be structured as short-term (1–3 years), medium-term (3–10 years), or long-term agreements (10–25 years).

The buyer must also define what percentage of total consumption should be covered through a PPA. This depends on the overall procurement strategy, the interaction between the PPA and other hedging products, and the volume that can be efficiently integrated without generating excessive imbalance costs.

The design of a PPA also involves decisions regarding the origin and characteristics of the associated generation asset. Some consumers may prioritize domestic projects aligned with ESG or industrial criteria over imported solutions that may offer more competitive pricing.

Asset type also has important implications for the risk profile and sustainability impact of the contract. A new project (greenfield) generally delivers greater additionality and more visible sustainability impact, although it also involves higher development and execution risks. Existing assets (brownfield), by contrast, may offer more mature structures with lower operational risk.

Another central element in PPA structuring is the pricing formula. Some contracts establish a fully fixed price throughout the agreement term, while others include partial indexation mechanisms linked to inflation, labor costs, or operational expenses.

Ultimately, the value of a PPA depends on how effectively the contract adapts to the buyer’s consumption profile, procurement strategy, and risk objectives.

It is important to understand that a PPA is not a standard product, but rather a combination of multiple decisions. From the technology to the pricing structure, including the volume, the type of delivery or the duration of the contract, each element can be configured differently depending on the buyer’s needs and the market’s supply options.

In practice, this means that there is no single PPA model, but rather multiple possible combinations. And it is precisely this flexibility that means their evaluation, comparison and structuring require technical, economic and risk analysis.

How to Calculate the Real Value of a PPA?

Once the contract structure has been defined, the next step is evaluating its true economic value.

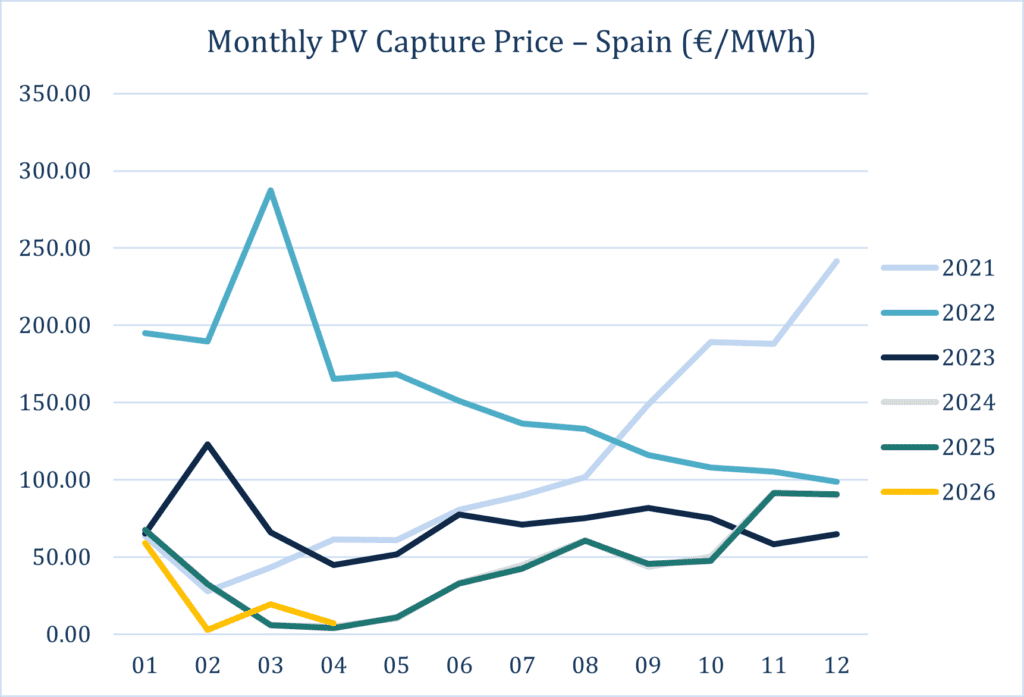

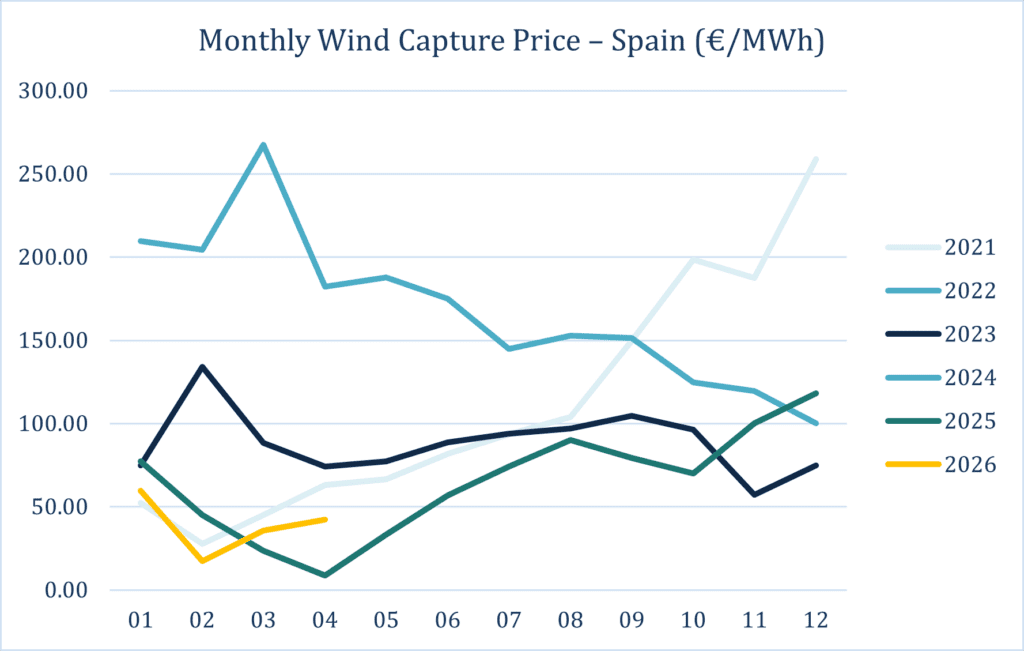

PPA valuation is typically based on the capture price, meaning the average price captured by renewable generation during the hours in which the asset produces electricity. Its estimation depends not only on expected future price levels but also on the shape and volatility of the forward price curve.

As a result, two scenarios with the same average annual price may generate significantly different capture prices.

As a result, two scenarios with the same average annual price may generate significantly different capture prices.

Moreover, the economic value of a PPA does not depend solely on the price of generated energy, but also on shaping and balancing costs. When renewable generation profiles do not match actual consumption patterns, additional energy must be bought or sold on the market to compensate for hourly deviations.

On the seller side, the minimum acceptable price is closely linked to the LCOE (Levelized Cost of Energy), representing the average cost of generation over the asset’s lifetime. In practice, producers cannot sustainably sell below this threshold without compromising project profitability.

Finally, PPA valuation should include sensitivity analyses and market scenarios. Future demand evolution, renewable penetration, gas prices, and CO₂ costs may significantly alter electricity prices and the economic value of the contract over time.

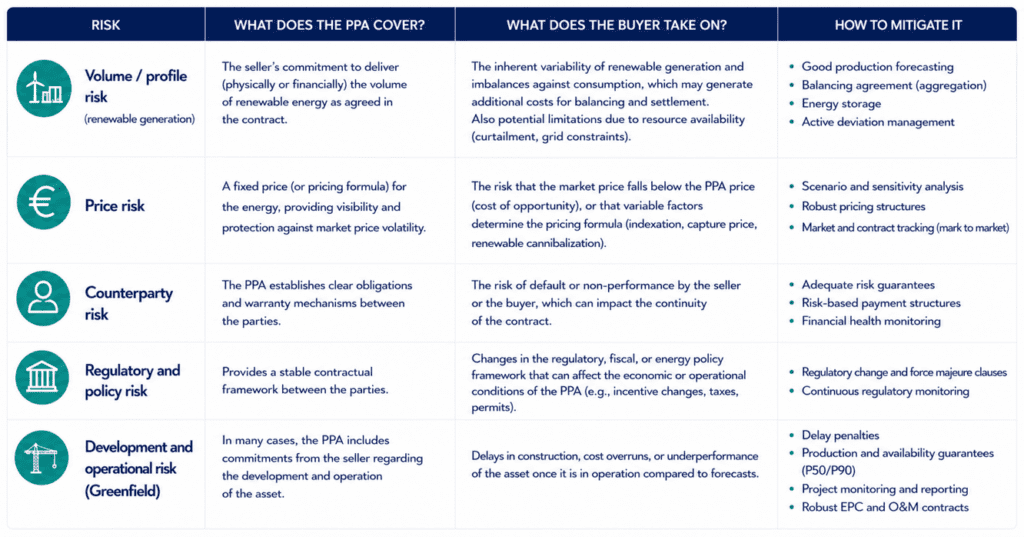

Key Risks: What You Hedge… and What You Take On

Although PPAs reduce exposure to electricity market volatility and provide greater budget visibility, they also introduce risks that must be carefully assessed before contract signature.

One of the main risks is volume or profile risk. Renewable generation is inherently variable and weather-dependent, meaning it may not perfectly match the buyer’s actual consumption profile. This can create energy surpluses or additional market purchases, increasing costs.

There is also price risk. While a PPA protects against rising market prices, it may also generate opportunity costs if electricity prices fall for an extended period, making the agreed price less competitive than spot or forward market alternatives.

Counterparty risk must also be considered. Since PPAs are long-term agreements, the financial strength of both the producer and the buyer is essential. Financial deterioration on either side may impact contract performance or trigger additional collateral requirements.

In greenfield projects, operational and construction risks are particularly relevant. Delays in commissioning, underperformance, or technical issues may affect energy delivery and alter the contract’s expected economic balance.

Regulatory risk should not be overlooked either, as changes in energy regulation may directly impact PPA conditions and economics.

For this reason, evaluating a PPA requires a comprehensive risk perspective that goes well beyond analyzing the offered price.

Negotiation and Execution: A Critical Process

Once the economic structure and risk profile of the PPA have been validated, the negotiation and contract execution phase begins. At this stage, the objective is no longer limited to defining a competitive price, but rather ensuring that the allocation of risks, responsibilities, and flexibility between the parties is consistent with the objectives of the agreement.

Far from being a mere formality, PPA negotiation is a complex process that can extend over several months. It involves multiple disciplines and stakeholders, ranging from commercial teams to legal and financial advisors responsible for ensuring that the contract accurately reflects the obligations and exposures assumed by each party.

During this phase, key elements such as the pricing structure, volume commitments, physical or financial delivery conditions, balancing cost allocation, financial guarantees, and force majeure or early termination mechanisms are negotiated.

In greenfield projects, negotiations also typically include aspects related to the development and construction of the asset, such as the expected Commercial Operation Date (COD) and penalties associated with delays.

The timing of execution also plays a significant role, as changes in electricity markets or financing costs may directly affect the value of the agreement for both parties.

For this reason, specialized support is essential not only to optimize the economic conditions of the contract, but also to properly identify, quantify, and mitigate the risks associated with a long-term contractual relationship.

After Signing: Continuous PPA Management

Signing a PPA is not the end of the process, but rather the beginning of an ongoing monitoring and contract management phase.

One of the first aspects to monitor is whether the asset is performing according to the assumptions defined in the business plan, and whether its generation profile remains aligned with the consumer’s procurement and hedging strategy.

It is also essential to verify whether the plant is meeting the guaranteed production levels established in the PPA and the generation forecasts used during the valuation phase. Significant deviations from these assumptions may lead to additional balancing costs, residual market exposure, or even contractual impacts depending on the agreed structure.

Beyond the economic dimension, measuring the sustainability impact associated with the contract is becoming increasingly important. In particular, the calculation of avoided CO₂ emissions makes it possible to quantify the real contribution of the PPA to the company’s decarbonization and ESG reporting objectives.

Finally, PPA management also involves monitoring contractual and financial aspects such as financial guarantees, compliance with milestones and contractual deadlines, and the management of Guarantees of Origin (GoOs).

In practice, post-signature PPA management requires continuous monitoring of both the operational performance of the asset and the economic and contractual evolution of the agreement.

Evaluating and managing a PPA goes far beyond comparing a price expressed in €/MWh. It requires understanding consumption profiles, market dynamics, price curves, associated risks, contractual structures, and the expected evolution of the electricity system. Ultimately, it involves making strategic decisions in an increasingly complex and volatile energy environment.

Precisely in this context, at Haya Energy Solutions we support our clients throughout every stage of the process: from analysis and structuring to negotiation and ongoing PPA management. Our approach combines market analysis, modelling, and technical and regulatory expertise with the objective of identifying the solution best suited to each company’s energy strategy, risk profile, and business objectives.

And this is only the beginning. In our next newsletter, we will take a closer look at a market player that is becoming increasingly relevant in the energy sector: the aggregator. Our expert Céline Haya will share her perspective on how these models operate, the value they provide, and why they are gaining prominence in the energy transition.

Irene Sánchez-Haro Montero