On Saturday, the US and Israel launched coordinated strikes on Iran and within 48 hours the conflict had spilled across the region: Iran retaliated with attacks targeting Israel and US military installations in the Gulf, while Israel expanded operations toward southern Lebanon amid Hezbollah activity.

Energy infrastructure is now directly in the line of fire. Saudi Arabia’s Ras Tanura refinery (Saudi Arabia’s largest domestic refinery with a capacity of 550,000 barrels per day) was hit and shut as a precaution after a drone strike, and QatarEnergy halted LNG production after attacks on facilities at Ras Laffan (Qatar’s main LNG hub) and Mesaieed (hosts large-scale NGL, refining and petrochemical facilities supporting Qatar’s downstream gas output).

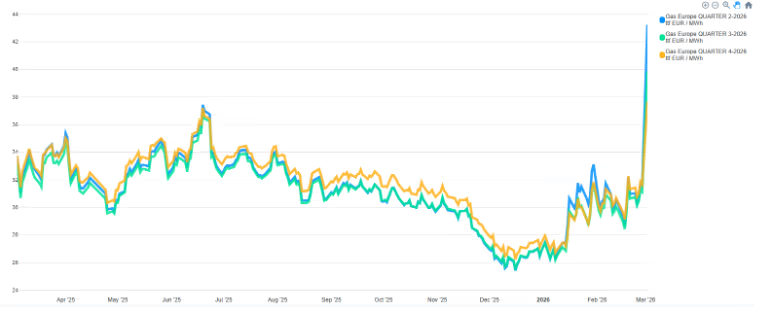

Markets repriced immediately: TTF Q2-26 moved from ~€31.7/MWh (27th Feb) to ~€53/MWh (3rd Mar), with power forwards also higher across DE/FR/ES.

What to expect if the conflict continues?

- What changed over the weekend: a regional escalation with direct energy implications

Saturday saw coordinated US–Israel strikes across Iran, followed by Iranian retaliation including attacks on US military installations in the Gulf. By early week, the conflict broadened involving Lebanon/Hezbollah and Israeli actions in southern Lebanon.

- The key energy shocks now in play

- Saudi refining disruption: Saudi Arabia’s Ras Tanura — widely reported as the kingdom’s largest domestic refinery — was shut after a drone strike (precautionary shutdown).

- Qatar LNG production halted: QatarEnergy stated it ceased LNG production and associated products after attacks on facilities at Ras Laffan and Mesaieed.

- Hormuz shipping risk: there is mixed messaging on whether the Strait is formally “closed,” but shipping conditions have clearly deteriorated — major maritime insurers have moved to cancel war-risk cover, and multiple vessels have paused/anchored in or near Hormuz, tightening logistics even without an official blockade.

- Market impact so far: gas and power up, but gas-led repricing compresses CSS

In just a few sessions, the forward curves spiked sharply higher, led by gas. From 27 Feb to 3 Mar, TTF jumped from ~€31–32/MWh to €~€43/MWh across Q2-26, i.e. roughly +11% (Q2), +8.6% (Q3) and +5.85% (Q4), marking a clear risk-premium peak on the back of supply/security headlines.

From 27 Feb to 2 Mar, power forwards also rose, but less aggressively than gas: for example Germany gained +12.6% in Q2 (70.7→83.3 €/MWh) and +8.3% in Q4 (93.6→101.9), while France was +3.2% in Q2 (21.5→24.7) and +2.3% in Q3 (33.3→35.7); Spain moved about +10% in Q2 (28.8→31.7) and Q3 (59.6→65.5).

The result is that the gas-led repricing mechanically compresses clean spark spreads, because fuel costs reprice faster than the power output they underpin.

- If the disruption lasts: the “scale” reference from Oxford/OIES

It is worth stressing the physical constraint: with the exception of small LNG deliveries to Kuwait, virtually all LNG exports from Qatar and the UAE transit the Strait of Hormuz. Qatar was the world’s second-largest LNG exporter in 2025 with >112 bcm of exports, while the UAE exported around 7 bcm; in total, just over 112 bcm of LNG transited Hormuz in 2025, close to 20% of global LNG trade. Crucially, there are no meaningful alternative routes to bring Qatar/UAE LNG to market if Hormuz transit is impaired. Qatar can supply piped gas to the UAE and Oman via the Dolphin pipeline (~20.5 bcm in 2025), but spare capacity is limited, and Oman’s LNG export terminals were running close to 100% utilisation, leaving little “workaround” capacity in the region.

If the conflict drags on and shipping risk in Hormuz becomes sustained, the market is facing a genuinely systemic LNG shock: around ~20% of global LNG trade transits the Strait of Hormuz, so any prolonged disruption quickly forces Asia and Europe into a bidding war for marginal cargoes. Moreover, storage levels in Europe are relatively low, making the summer refilling campaign particularly complex and highly sensitive to any additional pressure on supply.

In that type of stress, hub prices can plausibly move into €85–90/MWh as a first “severe but orderly” level and if the disruption escalates further or lasts long enough to drain storage materially, the upper tail starts to resemble the Ukraine crisis regime.